CKYC Registry

-

Customer Service Contact us Service request Locate a branch

Find all the help you need

Scan the QR, get our app, and find help on your fingertips

Help CenterSupport topics, Contact us, FAQs and more

-

Login

Login

Are you ready for an upgrade?

Login to the new experience with best features and services

-

Login

Are you ready for an upgrade?

Login to the new experience with best features and services

- Accounts

-

Deposits

IDFC FIRST Bank Deposits

View all Deposits -

Loans

IDFC FIRST Bank Loans

View all Loans - Wealth & Insure

-

Payments

IDFC FIRST Bank Payments

View all Payments -

Cards

IDFC FIRST Bank Cards

View all Cards - Blogs

- Corporate Account

-

Cash Management Services

IDFC FIRST Bank Cash Management Services

View all Cash Management Services - Supply Chain Finance

-

Corporate Lending

IDFC FIRST Bank Lending

View all -

Treasury

IDFC FIRST Bank Treasury

See more details - NBFC Financing

Help Center

Support topics, Contact us, FAQs and more

Accounts

- IDFC FIRST Bank Accounts

-

Savings Account

-

Corporate Salary

Account -

Senior Citizens

Savings Account -

First Power

Account -

Current Account

-

NRI Savings

Account -

TASC Institutional

Account -

Savings Account

Interest Calculator

Deposits

- IDFC FIRST Bank Deposits

-

Fixed Deposit

-

Recurring Deposit

-

NRI Fixed Deposit

-

Safe Deposit Locker

-

FD Calculator

-

RD Calculator

Loans

- IDFC FIRST Bank Loans

-

Personal Loan

-

Consumer Durable

Loan -

Home Loan

-

Business Loan

-

Professional Loan

-

Education Loan

-

New Car Loan

-

Pre-owned Car Loan

-

Two Wheeler Loan

-

Pre-owned Two

Wheeler Loan -

Commercial Vehicle

Loan -

Gold Loan

-

Loan Against Property

-

Loan Against Securities

-

Easy Buy EMI card

-

Personal Loan

EMI Calculator -

Education Loan

EMI Calculator -

Home Loan

EMI Calculator

Wealth & Insure

- IDFC FIRST Bank Wealth & Insure

-

FIRST Select

-

FIRST Wealth

-

FIRST Private

-

Mutual Funds

-

Sovereign Gold Bond

-

Demat Account

-

Term Insurance

-

Life Insurance

-

Health Insurance

-

General Insurance

-

Bonds

-

Loan Against

Securities -

Portfolio Management

Service

Payments

- IDFC FIRST Bank Payments

-

FASTag

-

Credit Card

Bill Payments -

UPI

-

Funds Transfer

-

Forex Services

-

Pay Loan EMI

Cards

- IDFC FIRST Bank Cards

-

Ashva :

Metal Credit Card -

Mayura :

Metal Credit Card -

FIRST Millennia

Credit Card -

FIRST Classic

Credit Card -

FIRST Select

Credit Card -

FIRST Wealth

Credit Card -

FIRST WOW!

Credit Card -

Deals

-

Debit Cards

-

Co-branded Cards

-

Credit Card

EMI Calculator -

FIRST Corporate

Credit Card -

FIRST Purchase

Credit Card -

FIRST Business

Credit Card

Premium Metal

- Premium Metal Credit Cards

-

AshvaLifestyle1% Forex₹2,999

-

MayuraLifestyleZero Forex₹5,999

-

FIRST PrivateInvite Only

0% Forex & Travel

- Best for travellers

-

MayuraZero ForexMetal₹5,999

-

Ashva1% ForexMetal₹2,999

-

FIRST WOW!Zero ForexTravelLifetime Free

-

FIRST SWYPTravel OffersEMI₹499

-

FIRST Select1.99% ForexLifestyleLifetime Free

-

FIRST Wealth1.5% ForexLifestyleLifetime Free

-

Club VistaraTravelLifestyle₹4,999

-

IndiGo IDFC FIRST Dual Credit CardTravelLifestyle₹4,999

Lifetime Free

- Max benefits, Free for life

-

FIRST Classic10X RewardsShoppingNever Expiring Rewards

-

FIRST Millennia10X RewardsShoppingNever Expiring Rewards

-

FIRST Select10X RewardsLifestyle1.99% Forex

-

FIRST Wealth10X RewardsLifestyle1.5% Forex

-

FIRST WOW!RewardsTravelZero Forex

-

LIC ClassicRewardsInsuranceShopping

-

LIC SelectRewardsInsuranceShopping

10X Rewards

- Reward Multipliers

-

AshvaLifestyleMetal₹2,999

-

MayuraLifestyleZero Forex₹5,999

-

FIRST ClassicNever Expiring RewardsShoppingLifetime Free

-

FIRST MillenniaNever Expiring RewardsShoppingLifetime Free

-

FIRST SelectNever Expiring RewardsLifestyleLifetime Free

-

FIRST WealthNever Expiring RewardsLifestyleLifetime Free

UPI Cards

- Rewards & Credit on UPI

-

FIRST Power+FuelUPI₹499

-

FIRST PowerFuelUPI₹199

-

FIRST EA₹NVirtual1% Cashback₹499

-

FIRST DigitalVirtualUPI₹199

-

IndiGo IDFC FIRST Dual Credit CardUPITravelDual cards

Fuel & Utility

- Fuel and Savings

-

FIRST PowerRewardsUPI₹199

-

FIRST Power+RewardsUPI₹499

-

LIC ClassicRewardsInsuranceShopping

-

LIC SelectRewardsInsuranceShopping

Showstopper

- Express and Flaunt

-

AshvaMetal1% Forex₹2,999

-

MayuraMetalZero Forex₹5,999

-

FIRST SWYPEMIOfferMAX₹499

-

FIRST MillenniaRewardsShoppingLifetime Free

Credit Builder

- FD Backed rewarding Credit Cards for all

-

FIRST EA₹NVirtualCashback₹499

-

FIRST WOW!Zero ForexTravelLifetime Free

-

CreditPro Balance TransferTransfer & SaveReduce InterestPay Smartly

More

NRI Savings Account

NRI Fixed Deposit

FOREX Solutions

- IDFC FIRST Bank NRI Forex Solutions

-

Send money to India-Wire transfer

-

Send money to India-Digitally

-

Send money abroad

-

Max Returns FD (INR)

Transfer to NRE

Corporate Account

Cash Management Services

Corporate Lending

Treasury

MSME Accounts

- IDFC FIRST Bank MSME Accounts

-

Platinum Current

Account -

Gold

Current Account -

Silver Plus

Current Account -

Merchant Multiplier

Account -

Agri Multiplier

Account -

TASC Institutional

Account -

Dynamic Current

Account -

World business

Account -

First Startup

Current Account

Trade Services

MSME Loan

- IDFC FIRST Bank Business Loans

-

Business Loan

-

Professional Loan

-

Loan Against Property

-

Business Loan for Women

-

Working Capital Loan

-

Construction Equipment Loan

-

Machinery Loan

-

Healthcare Equipment Loan

MSME Solutions

- IDFC FIRST Bank Business Solutions

-

Payment Solutions

-

Tax Payments

-

Doorstep Banking

-

Point of Sale (POS)

-

Escrow Accounts

-

NACH

-

Payment Gateway

-

UPI

-

Virtual Accounts

Offers

About Us

Investors

ESG

-

As per amendment in the Income Tax Rules, PAN or Aadhaar are to be mandatorily quoted for cash deposit or withdrawal aggregating to Rupees twenty lakhs or more in a FY. Please update your PAN or Aadhaar. Kindly reach out to the Bank’s contact center on 1800 10 888 or visit the nearest IDFC FIRST Bank branch for further queries.

-

-

Most Searched

Sorry!

We couldn’t find ‘’ in our website

Here is what you can do :

- Try checking the spelling and search

- Search from below suggestions instead

- Widen your search & try a more generic keyword

Suggested

Get a Credit Card

Enjoy Zero Charges on All Commonly Used Savings Account Services

Open Account Now

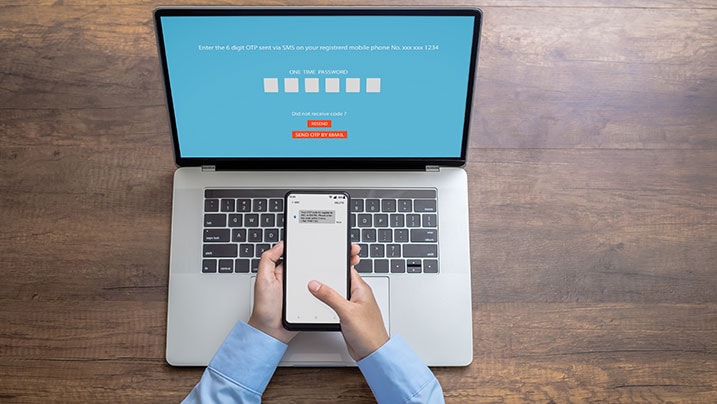

OTPs ensure your transactions are authenticated, thus protecting you from malpractices

Your credit card and debit card details are valuable. If someone gets access to them, they can use them to make transactions, leading to severe losses. Therefore, security is critical, and banks have provisions to ensure your details are protected. Two-step authentication is one of the measures used to protect your data.

As the name suggests, it has two steps: first, you must enter your PIN or password. Later, a four or six number is sent to your registered phone number. This number is called an OTP. Read on to find out more about it.

What is the meaning of OTP?

OTP is an acronym for One-time Password. It is usually generated when you are trying to make a transaction. OTP usually contains numbers, but it can also carry letters and alphanumeric characters in some cases.

OTP is commonly used as the second step of authentication as it is more secure than the static password you create. In the event of a hack, your static password might be compromised, but a dynamic OTP stays more secure.

Most banks equip their users with OTP protection nowadays. The same goes for IDFC FIRST Bank. IDFC FIRST Bank offers unparalleled security, allowing you to conduct transactions without worrying about data or money loss.

READ MORE

What is OTP in debit card transaction?

Your debit-cum-ATM card transactions require OTP in certain conditions. It won't ask for OTP when you pay at a POS terminal or withdraw small amounts of cash from an ATM. But some banks have enabled OTP authentication for higher cash withdrawals.

At the same time, OTP authentication is a must when you pay using your debit card online. It helps prevent online scams, hacks, and frauds.

What is OTP in credit card transactions?

Most of your credit card transactions require an OTP, except when paying at a POS machine. You must enter it to approve the transaction before it expires. The validity of OTPs differs, although they generally range from a few seconds to up to a minute and more.

OTPs can also be used as a single authentication method instead of a static password. It provides increased security as it is dynamic and challenging to guess.

International card transactions

International transactions using your credit or debit card don't require OTP authentication. The RBI has enforced OTP authentication only for domestic transactions, and international transactions do not come under their purview. Hence, the wise idea here is to disable international transactions or enable them only when you need to do an international transaction.

Other scenarios where OTP is needed

Banks may enforce OTP authentication for specific actions to increase security. Let's look at some of those scenarios.

1. When you log in to net or mobile banking

Access to your net or mobile banking portal means access to your bank account. Hence, the bank will require a solid and complex password for your login. In addition, most banks have OTP authentication as well.

2. When you change your banking password

If your banking password is compromised, the first thing hackers would do is change your banking password to restrict your access. To prevent this, banks require you to authenticate using an OTP when you try to change your password.

3. When you send money

Finally, banks will ask for OTP when you send money to another bank account online. UPI transactions are exempt from this because they have a restricted sending limit.

An OTP is an essential piece of security information that adds extra secrity to your banking. Never share your OTP with anyone, including bank officials, to steer clear of scams.

Benefits of a one-time password

One-time passwords offer enhanced security. They are unique for each login and expire quickly, within a few minutes, reducing the risk of unauthorised access. This adds an extra layer of protection, especially when combined with regular passwords. OTPs are easy to use and provide peace of mind, safeguarding your online accounts from potential breaches and unauthorised accesses.

Why would you use one-time passwords?

Using a one-time password is crucial due to its robust security benefits. An OTP can only be used once, enhancing your online safety. It safeguards your accounts from hackers who might steal your regular password through phishing attacks and other malpractices.

Even if someone obtains your OTP, they won't be able to misuse it after its single use. OTPs are particularly useful for sensitive transactions, like online banking or accessing private emails, where you want an extra layer of protection. They are a simple yet effective way to fortify your digital presence and keep your personal information secure.

How are one-time passwords created?

Creating one-time passwords involves an extensive process that enhances security for online accounts. These unique, temporary codes are generated using a combination of algorithms, ensuring they are nearly impossible to predict. Here is the step-by-step process of how OTPs are created:

1. Initial request: The process begins when a user attempts to log in to a secure online platform, such as a bank's website or an email account. The system detects this login attempt and recognises the need for an OTP.

2. Server-side algorithm: The server, or the online service's security system, runs a sophisticated algorithm to generate the OTP. This algorithm uses various factors to create a unique code for this specific login session.

3. Seed value: The algorithm often incorporates a "seed value." This is a random or time-based value that changes constantly. It serves as a starting point for generating the OTP.

4.Time-based OTP: In some cases, the OTP is time-based. The system considers the current time as a critical component in generating the code. This ensures that the OTP remains valid only for a short duration.

5. Unique code generation: Using the algorithm and seed value, the system generates a unique, one-time code.

6. Secure delivery: The OTP must be delivered securely to the user. This is typically done through a secure channel or trusted communication method to prevent interception by potential attackers. This code is typically sent to the user through a text message, email, or a dedicated OTP app.

7. User input: The user receives the OTP and enters it during the login process, proving their identity for that specific session.

8. Validation: The server validates the OTP entered by the user. It uses the same algorithm, seed value, and other factors to generate an expected OTP for this session. If the entered OTP matches the expected one, access is granted.

9. Expiration: To enhance security further, OTPs typically have a short lifespan. If not used within the designated time frame, they become invalid, adding an extra layer of protection.

10. Single use: Crucially, OTPs can only be used once. After successful validation or if the OTP expires, it becomes useless, thwarting any attempts by cybercriminals to reuse it.

11. Security benefits: The combination of complex algorithms, time-sensitive elements, and single-use nature makes OTPs a formidable barrier against unauthorised access.

What is Single-Factor Authentication (SFA)?

Single-Factor Authentication (SFA) is a basic method used to confirm a person's identity when accessing digital systems or online accounts. It relies on just one piece of information or factor to grant access. Typically, this single factor is a password or a PIN (Personal Identification Number).

Here's how it works. When you create an account on a website or system, you choose a password or PIN, which serves as your unique identifier. To access your account, you enter this password or PIN when prompted. If the entered password or PIN matches the one stored on the system, you are granted access.

However, SFA has limitations. It's less secure compared to Two-Factor Authentication (2FA) because it relies solely on something you know (the password or PIN). If someone else discovers or guesses your password, they could potentially gain unauthorised access to your account.

To bolster security, many organisations now encourage or require the use of 2FA, which combines two factors, like something you know (password), something you have (a smartphone), or something you are (biometrics) for enhanced protection.

What is Two-Factor Authentication (2FA)?

As mentioned earlier, Two-Factor Authentication (2FA) is an extra layer of security for online accounts. It requires two different pieces of information to confirm your identity. Typically, you start with your password (something you know) and then add a second factor, often a one-time code sent to your smartphone (something you have). This ensures that even if someone knows your password, they can't access your account without the second factor. 2FA greatly enhances online security by making it much harder for unauthorised individuals to gain access to your personal information and accounts.

Disclaimer

The contents of this article/infographic/picture/video are meant solely for information purposes. The contents are generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. The information is subject to updation, completion, revision, verification and amendment and the same may change materially. The information is not intended for distribution or use by any person in any jurisdiction where such distribution or use would be contrary to law or regulation or would subject IDFC FIRST Bank or its affiliates to any licensing or registration requirements. IDFC FIRST Bank shall not be responsible for any direct/indirect loss or liability incurred by the reader for taking any financial decisions based on the contents and information mentioned. Please consult your financial advisor before making any financial decision.

The features, benefits and offers mentioned in the article are applicable as on the day of publication of this blog and is subject to change without notice. The contents herein are also subject to other product specific terms and conditions and any third party terms and conditions, as applicable. Please refer our website www.idfcfirstbank.com for latest updates.