CKYC Registry

-

Customer Service Contact us Service request Locate a branch

Find all the help you need

Scan the QR, get our app, and find help on your fingertips

Help CenterSupport topics, Contact us, FAQs and more

-

Login

Login

Are you ready for an upgrade?

Login to the new experience with best features and services

-

Login

Are you ready for an upgrade?

Login to the new experience with best features and services

- Accounts

-

Deposits

IDFC FIRST Bank Deposits

View all Deposits -

Loans

IDFC FIRST Bank Loans

View all Loans - Wealth & Insure

-

Payments

IDFC FIRST Bank Payments

View all Payments -

Cards

IDFC FIRST Bank Cards

View all Cards - Blogs

- Corporate Account

-

Cash Management Services

IDFC FIRST Bank Cash Management Services

View all Cash Management Services - Supply Chain Finance

-

Corporate Lending

IDFC FIRST Bank Lending

View all -

Treasury

IDFC FIRST Bank Treasury

See more details - NBFC Financing

Help Center

Support topics, Contact us, FAQs and more

Accounts

- IDFC FIRST Bank Accounts

-

Savings Account

-

Corporate Salary

Account -

Senior Citizens

Savings Account -

First Power

Account -

Current Account

-

NRI Savings

Account -

TASC Institutional

Account -

Savings Account

Interest Calculator

Deposits

- IDFC FIRST Bank Deposits

-

Fixed Deposit

-

Recurring Deposit

-

NRI Fixed Deposit

-

Safe Deposit Locker

-

FD Calculator

-

RD Calculator

Loans

- IDFC FIRST Bank Loans

-

Personal Loan

-

Consumer Durable

Loan -

Home Loan

-

Business Loan

-

Professional Loan

-

Education Loan

-

New Car Loan

-

Pre-owned Car Loan

-

Two Wheeler Loan

-

Pre-owned Two

Wheeler Loan -

Commercial Vehicle

Loan -

Gold Loan

-

Loan Against Property

-

Loan Against Securities

-

Easy Buy EMI card

-

Personal Loan

EMI Calculator -

Education Loan

EMI Calculator -

Home Loan

EMI Calculator -

EMI Calculator

-

Personal Loan Eligibility Calculator

Wealth & Insure

- IDFC FIRST Bank Wealth & Insure

-

FIRST Select

-

FIRST Wealth

-

FIRST Private

-

Mutual Funds

-

Sovereign Gold Bond

-

Demat Account

-

Term Insurance

-

Life Insurance

-

Health Insurance

-

General Insurance

-

Bonds

-

Loan Against

Securities -

Portfolio Management

Service

Payments

- IDFC FIRST Bank Payments

-

FASTag

-

Credit Card

Bill Payments -

UPI

-

Funds Transfer

-

Forex Services

-

Pay Loan EMI

Cards

- IDFC FIRST Bank Cards

-

Ashva :

Metal Credit Card -

Mayura :

Metal Credit Card -

FIRST Millennia

Credit Card -

FIRST Classic

Credit Card -

FIRST Select

Credit Card -

FIRST Wealth

Credit Card -

FIRST WOW!

Credit Card -

Deals

-

Debit Cards

-

Co-branded Cards

-

Credit Card

EMI Calculator -

FIRST Corporate

Credit Card -

FIRST Purchase

Credit Card -

FIRST Business

Credit Card

Premium Metal

- Premium Metal Credit Cards

-

AshvaLifestyle1% Forex₹2,999

-

MayuraLifestyleZero Forex₹5,999

-

FIRST PrivateInvite Only

0% Forex & Travel

- Best for travellers

-

MayuraZero ForexMetal₹5,999

-

Ashva1% ForexMetal₹2,999

-

FIRST WOW!Zero ForexTravelLifetime Free

-

FIRST SWYPTravel OffersEMI₹499

-

FIRST Select1.99% ForexLifestyleLifetime Free

-

FIRST Wealth1.5% ForexLifestyleLifetime Free

-

Club VistaraTravelLifestyle₹4,999

-

IndiGo IDFC FIRST Dual Credit CardTravelLifestyle₹4,999

Lifetime Free

- Max benefits, Free for life

-

FIRST Classic10X RewardsShoppingNever Expiring Rewards

-

FIRST Millennia10X RewardsShoppingNever Expiring Rewards

-

FIRST Select10X RewardsLifestyle1.99% Forex

-

FIRST Wealth10X RewardsLifestyle1.5% Forex

-

FIRST WOW!RewardsTravelZero Forex

-

LIC ClassicRewardsInsuranceShopping

-

LIC SelectRewardsInsuranceShopping

10X Rewards

- Reward Multipliers

-

AshvaLifestyleMetal₹2,999

-

MayuraLifestyleZero Forex₹5,999

-

FIRST ClassicNever Expiring RewardsShoppingLifetime Free

-

FIRST MillenniaNever Expiring RewardsShoppingLifetime Free

-

FIRST SelectNever Expiring RewardsLifestyleLifetime Free

-

FIRST WealthNever Expiring RewardsLifestyleLifetime Free

UPI Cards

- Rewards & Credit on UPI

-

FIRST Power+FuelUPI₹499

-

FIRST PowerFuelUPI₹199

-

FIRST EA₹NVirtual1% Cashback₹499

-

FIRST DigitalVirtualUPI₹199

-

IndiGo IDFC FIRST Dual Credit CardUPITravelDual cards

Fuel & Utility

- Fuel and Savings

-

FIRST PowerRewardsUPI₹199

-

FIRST Power+RewardsUPI₹499

-

LIC ClassicRewardsInsuranceShopping

-

LIC SelectRewardsInsuranceShopping

Showstopper

- Express and Flaunt

-

AshvaMetal1% Forex₹2,999

-

MayuraMetalZero Forex₹5,999

-

FIRST SWYPEMIOfferMAX₹499

-

FIRST MillenniaRewardsShoppingLifetime Free

Credit Builder

- FD Backed rewarding Credit Cards for all

-

FIRST EA₹NVirtualCashback₹499

-

FIRST WOW!Zero ForexTravelLifetime Free

-

CreditPro Balance TransferTransfer & SaveReduce InterestPay Smartly

More

NRI Savings Account

NRI Fixed Deposit

FOREX Solutions

- IDFC FIRST Bank NRI Forex Solutions

-

Send money to India-Wire transfer

-

Send money to India-Digitally

-

Send money abroad

-

Max Returns FD (INR)

Transfer to NRE

Corporate Account

Cash Management Services

Corporate Lending

Treasury

MSME Accounts

- IDFC FIRST Bank MSME Accounts

-

Platinum Current

Account -

Gold

Current Account -

Silver Plus

Current Account -

Merchant Multiplier

Account -

Agri Multiplier

Account -

TASC Institutional

Account -

Dynamic Current

Account -

World business

Account -

First Startup

Current Account

Trade Services

MSME Loan

- IDFC FIRST Bank Business Loans

-

Business Loan

-

Professional Loan

-

Loan Against Property

-

Business Loan for Women

-

Working Capital Loan

-

Construction Equipment Loan

-

Machinery Loan

-

Healthcare Equipment Loan

MSME Solutions

- IDFC FIRST Bank Business Solutions

-

Payment Solutions

-

Tax Payments

-

Doorstep Banking

-

Point of Sale (POS)

-

Escrow Accounts

-

NACH

-

Payment Gateway

-

UPI

-

Virtual Accounts

Offers

About Us

Investors

ESG

-

As per amendment in the Income Tax Rules, PAN or Aadhaar are to be mandatorily quoted for cash deposit or withdrawal aggregating to Rupees twenty lakhs or more in a FY. Please update your PAN or Aadhaar. Kindly reach out to the Bank’s contact center on 1800 10 888 or visit the nearest IDFC FIRST Bank branch for further queries.

-

-

Most Searched

Sorry!

We couldn’t find ‘’ in our website

Here is what you can do :

- Try checking the spelling and search

- Search from below suggestions instead

- Widen your search & try a more generic keyword

Suggested

Get a Credit Card

Enjoy Zero Charges on All Commonly Used Savings Account Services

Open Account Now

History

IDFC FIRST Bank was founded by the merger of Erstwhile IDFC Bank and Erstwhile Capital First on December 18, 2018.

Erstwhile IDFC BANK LTD.

IDFC Limited was set up in 1997 to finance infrastructure, focusing primarily on project finance and mobilization of capital for private sector infrastructure development. Whether it is financial intermediation for infrastructure projects and services, whether adding value through innovative products to the infrastructure value chain or asset maintenance of existing infrastructure projects, the company focused on supporting organisations to get the best return on investments. The Company’s ability to tap global as well as Indian financial resources made it the acknowledged experts in infrastructure finance. Dr. Rajiv Lall joined the company in 2005 and successfully expanded the business to Asset Management, Institutional Broking, and Infrastructure Debt Fund. He applied for a commercial banking license to the RBI in 2013. In 2014, the Reserve Bank of India (RBI) granted an in-principle approval to IDFC Limited to set up a new bank in the private sector. Following this, the IDFC Limited divested its infrastructure finance assets and liabilities to a new entity - IDFC Bank- through demerger. Thus, IDFC Bank was created by demerger of the infrastructure, lending business of IDFC to IDFC Bank in 2015.

The bank was launched through this demerger from IDFC Limited in November 2015. During the subsequent three years, the bank developed a strong and robust framework including strong IT capabilities for scaling up the banking operations. The Bank designed efficient treasury management system for its own proprietary trading, as well as for managing client operations. The bank started building Corporate banking businesses. Recognizing the change in the Indian landscape, emerging risk in infrastructure financing, and the low margins in corporate banking, the bank launched retail business for assets and liabilities and put together a strategy to retailize its loan book to diversify and to increase margins. Since retail required specialized skills, seasoning, and scale, the Bank was looking for inorganic opportunities for merger with a retail lending partner who already had scale, profitability and specialized skills.

Erstwhile CAPITAL FIRST LTD.

Mr. Vaidyanathan who had built ICICI Bank’s Retail Banking business from 2000-2009 and was then the MD and CEO of ICICI Prudential Life Insurance Company in 2009-10, He quit the group for an entrepreneurial foray to acquire a stake in an existing NBFC with the stated intent of converting the NBFC to a commercial bank financing small businesses. During 2010-12, he acquired a significant stake in a real-estate financing NBFC through personal leverage, and launched businesses of financing small entrepreneurs and consumers. The NBFC wound down existing businesses and instead started businesses of financing such segments within consumer and micro-entrepreneurs that not financed by existing banks, by using alternative and advanced technology led models. He built a prototype for such financing (Rs 12000-Rs. 30,000, ~$300- $500), built a loan book of Rs. 770 crores ($130m, March 2011) within a year, and presented the proof of concept to many global private equity players for a Leveraged Management Buyout. In 2012, he concluded India’s largest Leveraged Management Buyout, got fresh equity of Rs. 100 crores into the company and founded Capital First as a new entity with new shareholders, new board, new business lines, and fresh equity infusion.

Between March 31, 2010 to March 31, 2018, the Company’s Retail Assets under Management increased from Rs. 94 crores ($14m) to Rs. 29,625 crores ($4.3 b, Sep 2018). The company financed seven million customers for Rs. 60,000 crores ($8.5b) through new age technology models. The company turned around from losses of Rs. 30 crore and Rs. 32 crores in FY 09 and FY 10 respectively, to PAT of Rs. 327 crores ($ 4.7b) by 2018, representing a 5-year CAGR increase of 56%. The loan assets grew at a 5-year CAGR of 29%. The ROE steadily rose from losses in 2010 to 15% by 2018. The market capitalization of the company increased ten-fold from Rs. 780 crores in March 2012 at the time of the MBO to over Rs. 8,282 crores in January 2018 at the time of announcement of the merger. As per its stated strategy, the company was looking out for a banking license to convert to a bank.

A New Bank

Growth is real only when it is sustainable and serves the long-term interest of stakeholders. An aspiration for accelerated and sustained growth paved the way for the merger of erstwhile IDFC Bank Ltd and erstwhile Capital First Ltd on December 18, 2018. Thus, a new bank with a new DNA was born – IDFC FIRST Bank. The merger is a milestone in the history of the two institutions and marks the end of one journey and beginning of a new one.

IDFC FIRST Bank is born to be distinctly different from what it was earlier. It has a renewed focus on retail business with an intent to fast-forward its growth trajectory, and to serve many more customer segments that are growth-drivers of the Indian economy. Our new bank fuses state-of-the-art technology superior liability platform of erstwhile IDFC Bank with analytics-led lending capabilities, the retail DNA and strong profitability track record of erstwhile Capital First. It enables both the institutions to expand capabilities and reach and to better serve customers. Thus, the merger sets the stage for the creation of a financially and strategically stronger entity. IDFC FIRST Bank now has a strong funded asset base of more than ₹ 2,31,000 crore with 82% in the Retail, Rural & MSME segment. Net Interest Margin has expanded from 1.6% in H1 FY19 to 6.0% in Q3-FY25. The Bank now enjoys a leading position in some of the retail asset segments. The Bank’s tech-driven liabilities platform is ready to grow exponentially with a new focus on expanding footprint across the nation.

As a Bank, our approach is to keep banking simple, easy to know and easy to understand. We enable people to save, borrow, invest, grow, and protect their wealth. Our service is characterised by digitisation, personalisation and customer-centricity, in addition to extensive physical reach. In addition to the exceptional strengths of erstwhile IDFC Bank, we derive the required expertise from the unique business model of erstwhile Capital First.It deploys its greenfield method of assessing credit risk – a strength that has enabled it to lend extensively to first-time borrowers and yet maintain a healthy asset quality that has withstood the challenges of economic cycles and policy changes.We are a people’s bank – for the salaried and self-employed, small businesses and micro-enterprises.With a specific emphasis on the underserved and first-time borrowers.The underserved segments are important to us. We also have the opportunity to bring these customers into the financial mainstream and touch their lives in a positive way

We believe an immense opportunity awaits us, as IDFC FIRST Bank starts to invest in customer-driven innovation that will create new liability products, new credit markets and new jobs – keeping in view the needs of a New India.By financing the growth of business and consumption, we not only participate in the growth of the country but also generate employment for millions. This, we believe, will lead to greater domestic production, greater consumption and will contribute to the virtuous cycle of growth of the nation. IDFC FIRST Bank is confident and ready to chart out its own destiny. It is now better positioned for growth in its business, deploy new digital channels, enter new markets and serve more customers.

New Mission

The new brand identity of IDFC FIRST Bank signifies growth and energy. It reflects the progressive spirit of our times. The symbolism behind our new identity is drawn from the theme of ‘progress’. Inspired by a forward-moving bar graph, it embodies a symbol of growth that can be seen and measured. The three bars stand for a threefold purpose - progress of the bank, progress of our customers and progress of the nation.

OUR VISION

To build a world class bank in India, guided by ethics, powered by technology, and be a force for social good.

OUR Mission

On a mission to build India's most customer friendly Bank!

OUR Values

Our Cultural Tenets to guide every action we take

Customer Focused

We put the customer’s interest first by putting ourselves in the customer’s situations and viewing things from their perspective.

Collaborative

We develop, maintain and strengthen relationships with both internal and external stakeholders.

Innovative

We constantly strive to innovate in the customer's interest.

Empowered

We trust our employees ability to be successful, especially at challenging new tasks; delegating responsibility and authority. Decisive Decisive We exercise best judgement by making sound and well-informed decisions.

Decisive

We exercise best judgement by making sound and well-informed decisions.

Action Oriented

We consistently demonstrate focus, initiative and energy to deliver our promise of delighting customers.

Our Founding Philosophy

The founding years, which we call the next five years, are particularly important, as the DNA we establish now will be hard to correct later. We will make every effort to sell the right products to customers, avoid mis-selling, avoid selling such third-party products that make wonderful fees for us but at the cost of expensive products for the customer. If we make a mistake, we will apologise and correct it. After all, we do not want to take this Bank to great heights in profits and profitability while having earned any penny that truly does not belong to us”

Strategy for the Bank

We plan to implant the erstwhile Capital First’s tried and tested model of financing small entrepreneurs and consumers (a retail franchise, growing at 29% per annum and 5-year profit CAGR of 55%, (FY 18 PAT grew by 37%)), on a bank platform, (IDFC Bank’s strong branch network of 580 and growing, excellent technology stack, quality internet and mobile banking, and strong rural presence).

Road leading to the Merger

An Integration Committee Meeting in progress.

The listing of IDFC FIRST Bank shares on NSE

Employees greeted the merger with great creativity and decorations across the country in all branches

Employees across the country in all branches greet the merger with celebrations on Day 1 - Dec 18, 2018

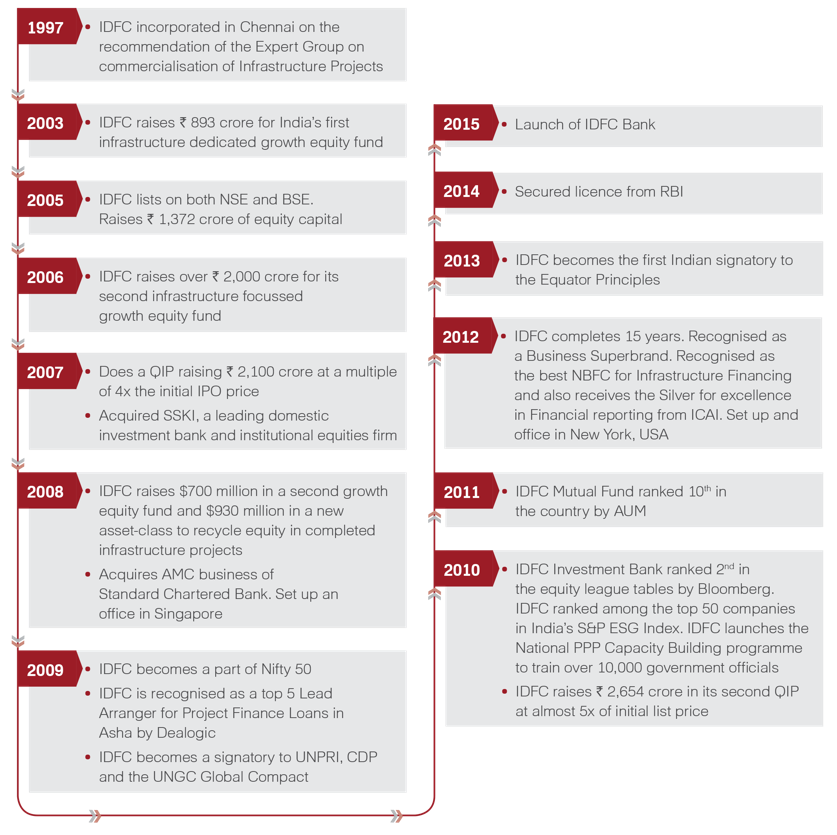

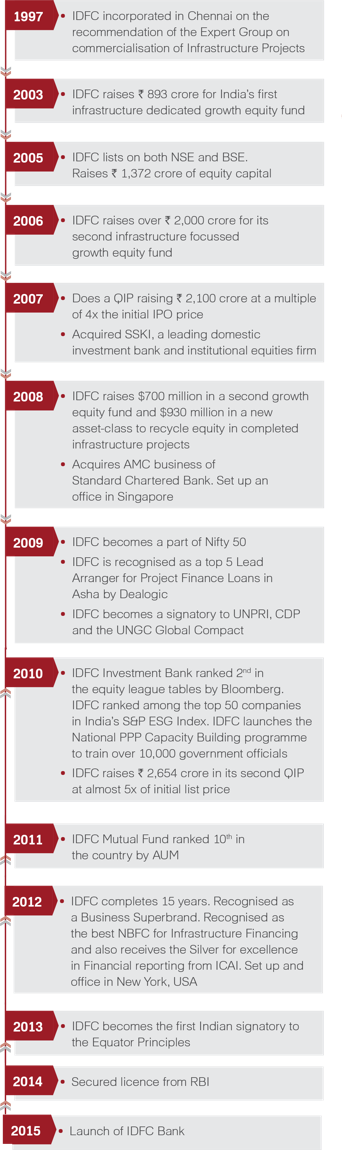

IDFC’S Evolution

In the News

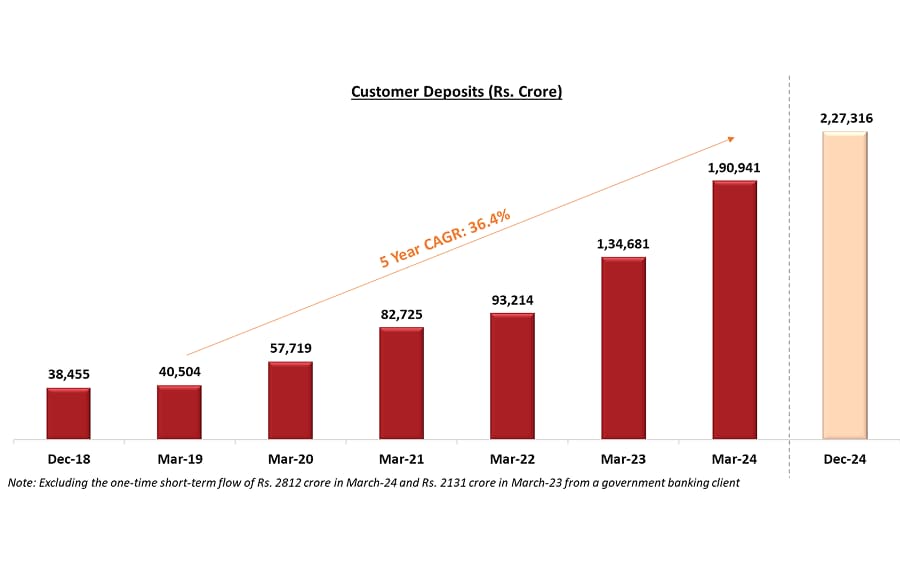

Total Customer Deposits (Retail Deposits + Wholesale Deposits) has grown strongly by 5 Year CAGR (Mar-19 to Mar-24) of 36%.

CASA Deposits has grown by 5 Year CAGR (Mar-19 to Mar-24) of 63%

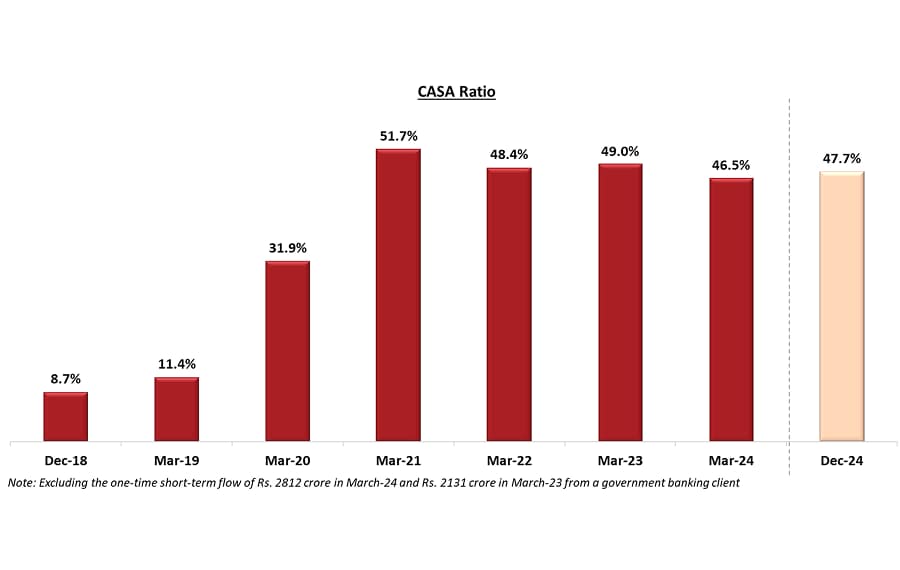

Our CASA ratio has risen from 8.7% in December, 31 2018 to 47.7% in December 31, 2024

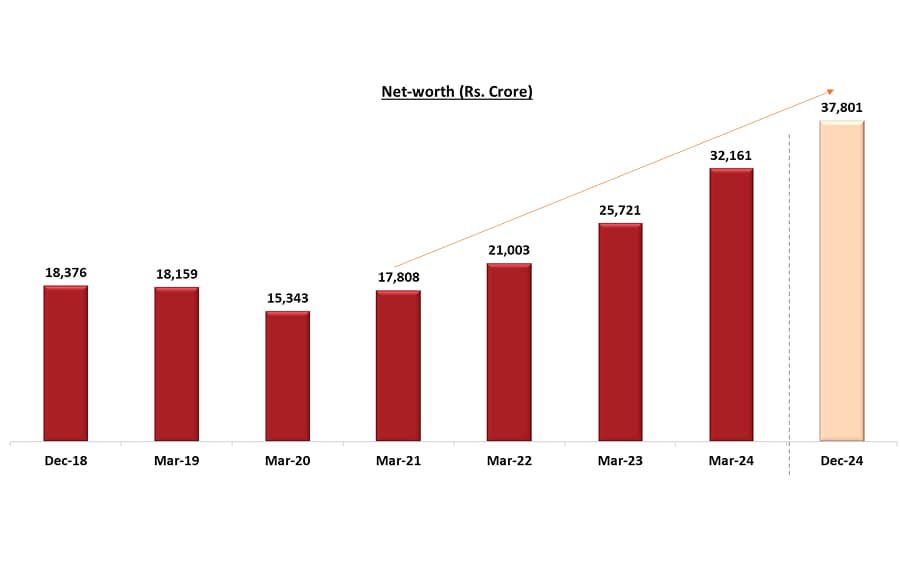

The Net-worth of the Bank has increased from Rs. 17,808 as of March 31, 2021 to Rs. 37,801 crore as on December 31, 2024